Matty’s Minute: An October Market Update

Photo By: Vance Fox Photography

Demand for mountain real estate has been propelled by a vast multitude of variables to unfathomable heights over the last 18 months. Such variables, many of which are non-economic, have begun to take a personality of their own in defining the performance of the local market.

The surge of Tahoe consumers that began in May of 2020 took its first break in the last month as conditions from nearby wildfires rendered the air unsafe. As the fires have given way to arguably the most beautiful season in Tahoe, this pause has given way to a period of catch-up. Pent-up demand has met the briefest of supply overhangs to produce solid velocity of new sales during a season that is “normally” the busiest of the year for local transactions.

Despite a pause that lasted nearly a full month, Q3 represented the busiest ever quarter for Tahoe Truckee real estate but for the same period in 2020 during which the local market reached a fever pitch. That 557 residential transactions equaled only 58% of the Q3 2020 figure speaks more to the fervor of the prior year than any slowdown. In fact, tight supply seems to be the only factor restraining the current market as both median and average pricing increased 20% over this period. Average days on market are approximately 50% fewer than during 2020.

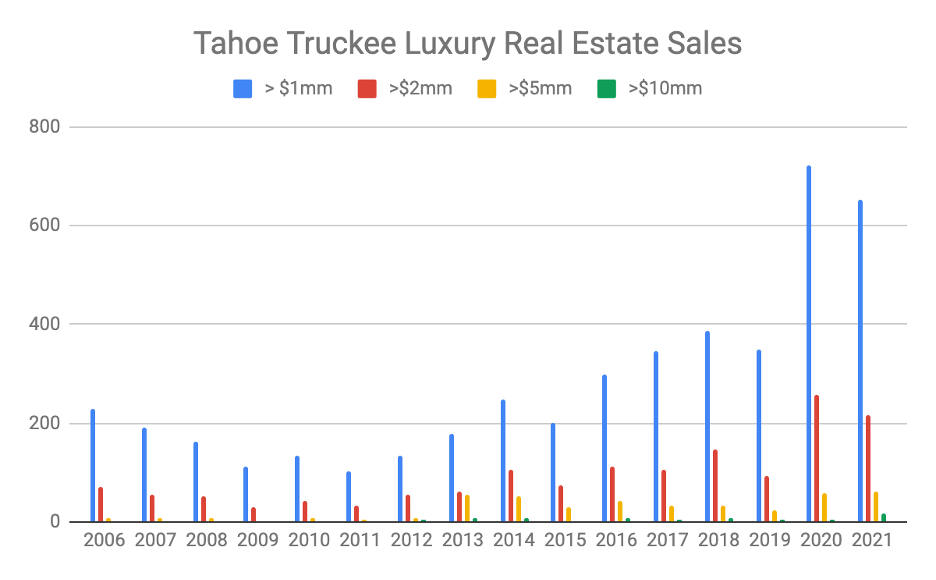

Notable within the market dynamic is the performance of luxury real estate. Amid surging pricing, the share of transactions above $1,000,000 has grown from 33% in 2020 to 47% during Q3. For greater context, despite almost 50% fewer transactions overall, the number greater than $1,000,000 is nearly 200 higher through the first nine months of this year. The number of transactions above $5,000,000 has doubled the quantity at this time last year and, remarkably, transactions greater than $10,000,000 are three times greater than the 12-month total in 2020 and represent nearly 33% of all transactions above that threshold all time.

Interestingly, eight of the ten highest priced transactions during Q3 were found in Martis Camp with the other two being Tahoe lakefronts at $10,000,000 and $35,000,000 respectively.

During the September pause, inventory crept up slightly to just under 2 months’ supply. This paucity is only slightly less ludicrous than 3–5-week supply maintained throughout most of 2020. The inventory that remains on the market is largely represented by opportunistic sellers seeking to capitalize on irrational purchasers. Average asking price is 180% higher than average sales price including 16 seeking more than $10,000,000 and a handful north of $40 million.

In years past, September and early October often yield the greatest number of new transactions as summer shopping merges with anticipation of winter. This often delivers peak closing in the latter stages of October and early November. With clear skies, cool temps and early season snow in the forecast, focus is shifting toward winter and resort-based properties where fractionally more supply exists. As such, we anticipate a strong close to 2021.

-Matty