Matty’s Minute: An October Market Update

Greetings;

Q3 has provided revealing data as to the trajectory of Tahoe Truckee real estate. Activity has tapered, and values have settled somewhat, however, supply remains modest because a very high percentage of homeowners are enjoying the use of their Tahoe properties. Thus, only those having purchased in the last year are at risk of being upside down. This is relative to basis and the general lack of distress in relation to mortgage burdens, which remain almost nil.

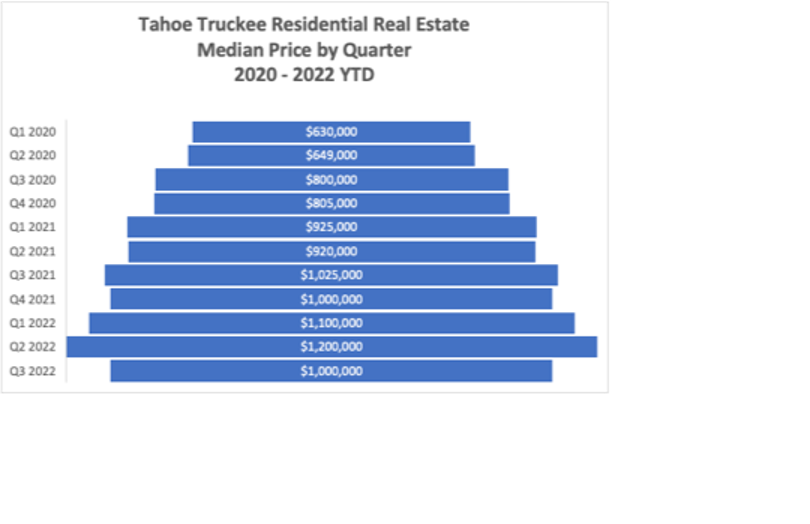

As is always the case, blanket generalizations never tell a complete story as specific micro-markets continue to appreciate while others settle into late 2021 valuations. Similarly, not all metrics are moving in unison. For example, average price peaked during Q1 2022 riding high on several premium sales including 10 eight-figure sales between Martis Camp and Tahoe lakefront. Median price continued to surge for one more quarter as median price rose to an all-time peak at $1,200,000 in Q2, despite activity in the elite tier cooling. This reveals a large volume of properties transacting within the middle tier of the local market as inventory began to loosen for the first time in several years.

Correspondingly, the increase in inventory has resulted in an uptick in the total numbers of transactions in each successive quarter this year.

In total, Q3 values precisely match the results from Q4, 2021 meaning any regression in pricing is giving back the gains from early this year when conditions were at the apex of competition with plentiful consumers fighting over historically scarce inventory.

Inventory peaked in August at just over 3 months’ supply; a rate of absorption that favors the seller despite being a quadrupling of supply from the beginning of the year.

Land sales have slowed at a much more significant level. Homesite sales in areas other than the most premium neighborhoods were already suffering while home sales continued to surge based upon building costs increasing at a rate greater than appreciation or inflation. As well, tight labor and supply chain disruptions rendered most projects out several years often eating up a large amount of the user’s lifespan for the finished home.

Reigniting consumer demand for vacant land requires a realignment of building costs and labor relative to the final home value in addition to a predictable market for the finished home. Communities in which land has most closely tracked the performance of new homes will suffer the least price erosion; Lahontan being the most notable where land has consistently sold for 10% - 15% the value of a new home.

The early weeks of Q4 are typically the apex for residential closings. The market has undeniably cooled from the fever pitch of the preceding two years, however an accurate snapshot of exactly how far the market will adjust is still undetermined.

As always, please contact me for more informations about current market dynamics and/or to have a listing consultation or a property tour today.